March held steady, mirroring February’s activity and signaling a stable, cautious market. Shifts this month were in tone and texture: publishers continued to favor high-concept adult fiction, with general, romance, and thriller categories all tracking consistently with prior months.

Non-fiction showed incremental growth, continuing its recovery from the post-holiday slowdown, especially in memoir, political commentary, and pop culture analysis. In the children’s space, Middle Grade edged back into view after several quiet months, though not dramatically, while YA remained consistent, with continued interest in fantasy-forward, emotionally resonant debuts.

March brought a noticeable contraction in debut deals across most major categories, following February’s broader openness to new voices. While total debut volume declined, the biggest changes came in where publishers chose to place their debut bets (spoiler: Thrillers are on the rise!)

Across genres, multi-book and multi-territory deals remained common, reflecting a focus on franchise potential and exportable properties. The big picture? March didn’t bring dramatic change, but confirmed the market’s current posture: measured, steady, and focused on high-confidence projects. Sounds like our publisher friends aren’t in much of a risk-taking mood!

March 2025 Genre Trends

Memoir continues to hold strong, sustaining the momentum it began building in February. These range from deeply personal stories to platform-driven narratives, often tied to broader cultural or political themes. Memoir is clearly still a comfort zone for nonfiction.

Spirituality surged quietly but meaningfully. This includes both traditional spiritual nonfiction and more contemporary takes on meaning, purpose, and personal transformation. It's a notable shift from February, when this category was barely visible.

There's a quiet but notable re-emergence of personal, spiritual, and poetic storytelling, especially when blended with memoir or visual formats.

Poetry is popular, reinforcing last month's signal that this once-niche format may be regaining ground, especially in hybrid formats (e.g., poetry-infused memoir or illustrated verse collections).

Graphic novels continued their reliable presence, especially in YA and MG categories. These often tie into visual storytelling trends and media crossover appeal.

Romantasy was up modestly from its near-absence in February, but still far below its late-2024 highs. This suggests a soft rebound, not a full resurgence. Publishers may be waiting to see what sticks before overcommitting to this crowded space…!

Romantasy and speculative subgenres aren’t gone, but they’re treading water — suggesting a more selective approach from editors.

Meanwhile, parenting nonfiction, new adult fiction, and YA nonfiction all remained nearly or completely absent — echoing the drop we saw in February. These categories may still be in cooldown mode, either due to filled acquisition slots or reader fatigue.

Practical nonfiction categories like parenting, self-help, and YA nonfiction may be in a temporary lull, signaling an opportunity for writers to sharpen positioning or explore alternative framing.

Overall, March reinforced the trend toward emotionally resonant, author-driven content with clear audience hooks — whether that's memoir, poetry, or the occasional romantasy rebound

March 2025 Debut Deal Trends

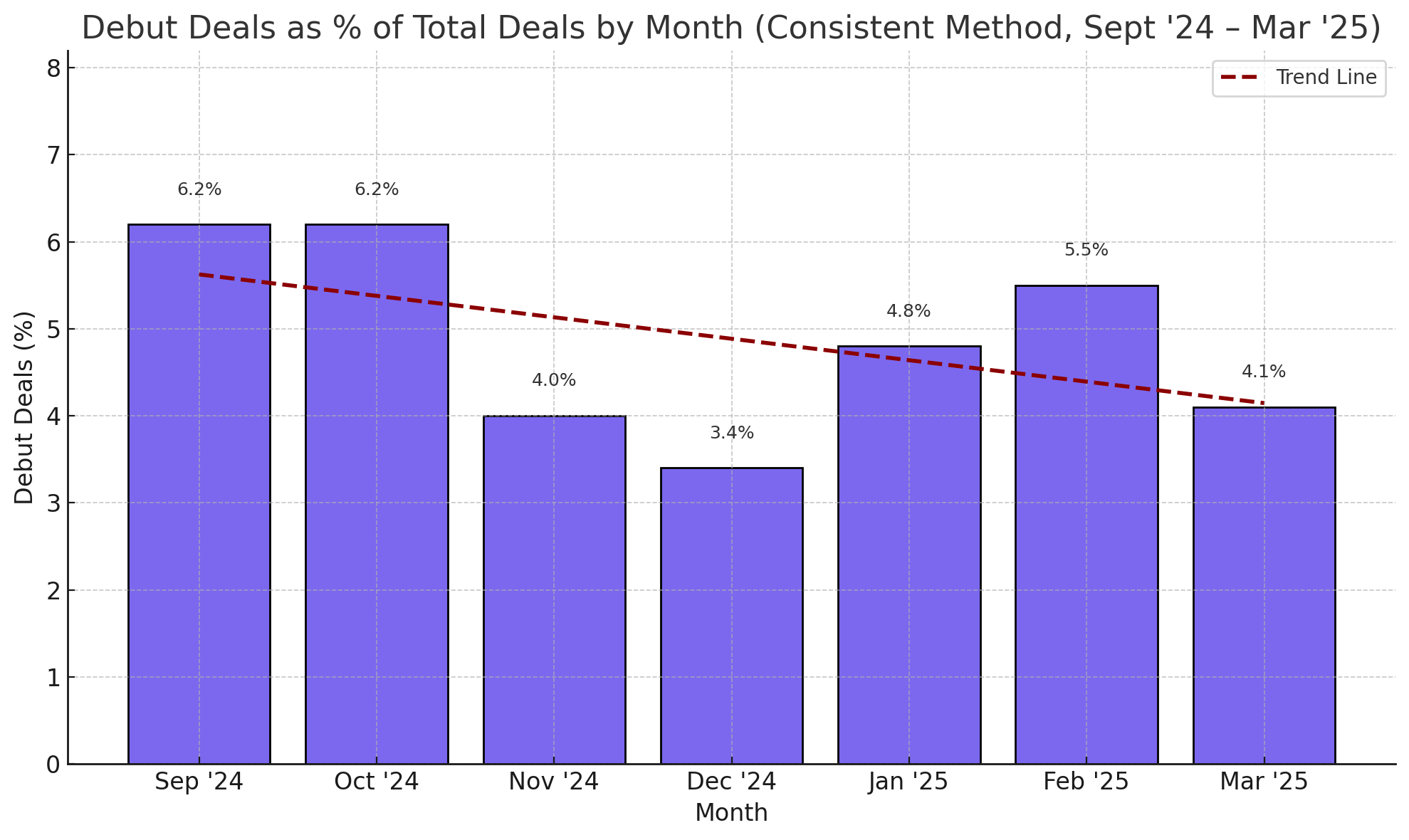

March saw a clear decline in debut acquisitions, with just over 50 debut deals, which marks a drop of over 25% from February. This marks the most selective month so far in 2025 for first-time authors.

Debut Deal Shifts in March: A Market Pullback

Following February’s broader openness to new voices, March brought a noticeable contraction in debut deals across most major categories. While total debut volume declined, the biggest changes came in where publishers chose to place their debut bets.

Adult Fiction: General saw the steepest drop.. While still the most active genre, the decrease signals a more selective posture, even for voice-driven commercial fiction.

Romance debuts plummeted in March, reversing what had looked like a promising February rebound. Whether this reflects market fatigue or seasonal reshuffling remains to be seen…!

Middle Grade Fiction— where did you go?! This gap continues a multi-month trend where MG debut activity remains sporadic at best.

YA Fiction remained fairly steady, suggesting continued editorial appetite for high-concept or emotionally resonant YA voices.

Conversely, Thriller debuts rose! While modest, the increase stands out against the broader slowdown, and may hint at renewed interest in psychological suspense and crime-driven narratives from first-time authors.

From the looks of things, publishers may be tightening the filter for first-time authors, especially in mainstream adult fiction and romance. However, opportunities still exist — particularly in thrillers and stable YA categories — for manuscripts with strong hooks and market clarity. If you're querying, this is the moment to lead with precision: genre identity, emotional resonance, and a clear audience pitch are more important than ever! (Duly noted)

International Market Trends

Mentions of UK, Germany, and France continued to lead geographic deal activity, consistent with their longstanding strength in rights acquisitions. While references to Spain, Brazil, and Japan were present, they were lower than in February — signaling a possible regional cooldown.

Asia saw subdued mentions overall, though Japan and China remained modestly represented in translation and co-edition deals, particularly around non-fiction and illustrated children's formats. The Netherlands and Italy maintained a light but steady presence.

Multi-book and multi-territory deals remain active, especially in commercial fiction, though the pace slowed slightly.

Children’s international rights continue to trail behind adult categories — a reversal from late 2024’s spike.

March’s quieter international profile suggests that many publishers may have finalized their foreign rights slates earlier in the quarter, with new activity likely to pick up after April.

Take note: Any changes in charts over time reflect a more reliable way of analyzing the data, that I’ll do my best to carry forward. Historical posts will not be updated. In most cases, broad trends remain the same.